At the 2010 G20 summit in Seoul, leaders recognized greater financial inclusion as a core component of global development in both rich and emerging economies, and established the Global Partnership for Financial Inclusion (GPFI). Following the recent GPFI meeting under Germany’s G20 Presidency over May 2-4, Annamaria Lusardi explores some of the costs of financial illiteracy, and makes the case for G20 leaders to expand financial literacy education services.

Only half of the adults in major advanced economies who use a credit card or borrow from a financial institution are financially literate. In emerging economies, financial literacy levels are even lower. And around the world, population subgroups—women, the poor, people with low formal education—trail in their financial knowledge, regardless of the strength of their countries’ economies.

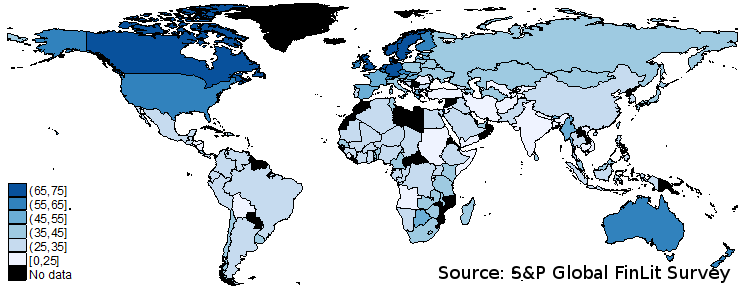

According to the new Standard & Poor’s Global Financial Literacy survey—the world’s largest and most comprehensive study of financial knowledge—we have reached a crisis stage. Financial literacy is not only very low in emerging countries, such as the BRICS, but it is also shockingly low in countries with well-developed financial markets and countries with high per-capita income. That includes the major advanced economies—among them the G7—where the use of financial products is widespread.

In order to make sound financial decisions, people must understand at least basic financial concepts. Yet the data shows that too much of the world’s population lacks the ability to make informed financial choices when it comes to saving, investing, borrowing, and more.

Financial knowledge is especially important during times when increasingly complex financial products are easily available to a wide range of the population. We are living in those times. As governments in many countries push to boost access to financial services, the number of people with bank accounts and credit products is rising rapidly. Changes in the pension landscape are transferring decision-making responsibility to workers who previously relied on their employers or governments to ensure their financial security after retirement. In the United States, where lawmakers are promising to revise an already complicated health insurance system, most Americans do not understand the precepts of insurance. In China, where credit card ownership has doubled since 2011, only half of credit card owners can perform simple calculations related to interest.

Financial ignorance carries a hefty price tag. Consumers who do not understand interest compounding, for example, spend more on transaction fees, run up bigger debts, and incur higher interest rates on loans. They also end up borrowing more and saving less.

The potential benefits of financial literacy, meanwhile, are manifold. People with strong financial skills do a better job planning and saving for retirement. Financially savvy investors are more likely to diversify risk by spreading funds across several ventures. They also earn more on their investments.

Until recently, a comparison of financial literacy across many countries was not possible. The Standard & Poor’s Ratings Services Global Financial Literacy Survey has opened the way to a comparable measure of financial literacy in more than 140 countries. The S&P Global FinLit Survey, for short, also links financial literacy to measures of financial inclusion provided by the Global Findex Database. These new data make it possible to examine financial knowledge worldwide and to assess the potential impact of what consumers do—or do not—know.

Financial literacy is measured through questions that assess basic knowledge of four fundamental concepts in financial decision-making: interest rates, interest compounding, inflation, and risk diversification. The S&P Global FinLit Survey findings are sobering. Worldwide, only 1-in-3 adults are financially literate. Or put in another way, some 3.5 billion adults globally fail to understand basic financial concepts.

Worldwide, there are striking similarities among the groups that are less likely to be financially literate. Irrespective of the level of income or the sophistication of the financial markets, women’s financial literacy levels are low—and that is true in almost all countries. This finding is important since roughly half the people on the planet are female. Worldwide, 30 percent of women are financially literate. That compares with 35 percent of men.

Income is another indicator. The rich have better financial skills than the poor. Some 31 percent of adults in the richest 60 percent of households in the major emerging economies are financially literate. In the poorest 40 percent of households, 23 percent of adults are financially literate. The size of the income gap is similar in the major advanced economies, although some suffer from even deeper inequality.

Access to Financial Services Carries Benefits; Poor Financial Literacy Dilutes Them

Financial literacy skills are important for people who use payment, savings, credit, and risk-management products. For many, opening an account at a bank or other financial institution—or using a mobile money-service provider—is an important first step to participation in the financial system. When people have financial accounts and use digital payments, they are better able to provide for their families, save money for the future, and survive economic shocks. According to the S&P Global FinLit Survey, financial account holders tend to be more financially savvy (although plenty of them still lack financial skills). Globally, 38 percent of account-owning adults are financially literate, as are 57 percent of account owners in major advanced economies and 30 percent in major emerging economies.

But there is a drawback. Account owners without financial knowledge may not fully benefit from what their accounts have to offer. Even more, this access to financial products can propel them into financial disaster, such as high debt or bankruptcy.

Take savings as an example. Globally, 57 percent of adults save money, but just 27 percent use a formal financial institution, such as a bank, to do so. Others rely on more precarious and less lucrative alternatives, such as informal savings groups or stuffing cash under a mattress. Only 42 percent of account owners worldwide use their accounts to save, and 45 percent of these adult savers are financially literate. Given the benefits derived from using financial services, it is important to ensure that people are capable of managing those services to their advantage.

Financial literacy challenges are universal, confronting developing economies and advanced economies alike. Policymakers should build strong consumer protection regimes to safeguard citizens from financial abuse and provide a smooth market environment. They should also take steps to ensure access to financial education.

School seems a great place to start, both for its capacity to reach large segments of the population (including women) and because individuals lacking financial knowledge are less likely to learn it from families or peers. Low-income groups can be targeted by embedding financial education programs in some of the programs already offered to them.

The message of the G20 Summit is “shaping an interconnected world.” As these influential leaders convene to empower people around the globe, addressing the challenges of financial literacy promises a high-impact multiplier effect.

Map 1: Global Variations in Financial Skills

The author organized and moderated the session Digitising Finance and Financial Literacy—Growing Importance in a Digital Landscape and a Low Interest Rate Environment at the G20 conference in Wiesbaden, Germany, on January 25-26, 2017. This article is an abridged version of the research described in this paper.

Schreibe einen Kommentar